Q3 2026 Market Outlook

Q2 of 2026 is shaping up better than we expected in our 2026 market outlook. Despite the noise around the globe and here in the U.S., based on CNBC-reported data, the S&P 500 is sitting roughly 8.4% positive on the year as of this writing. Similar to our outlook for 2026, but frankly better than anticipated so far.

The Markets So Far in 2026

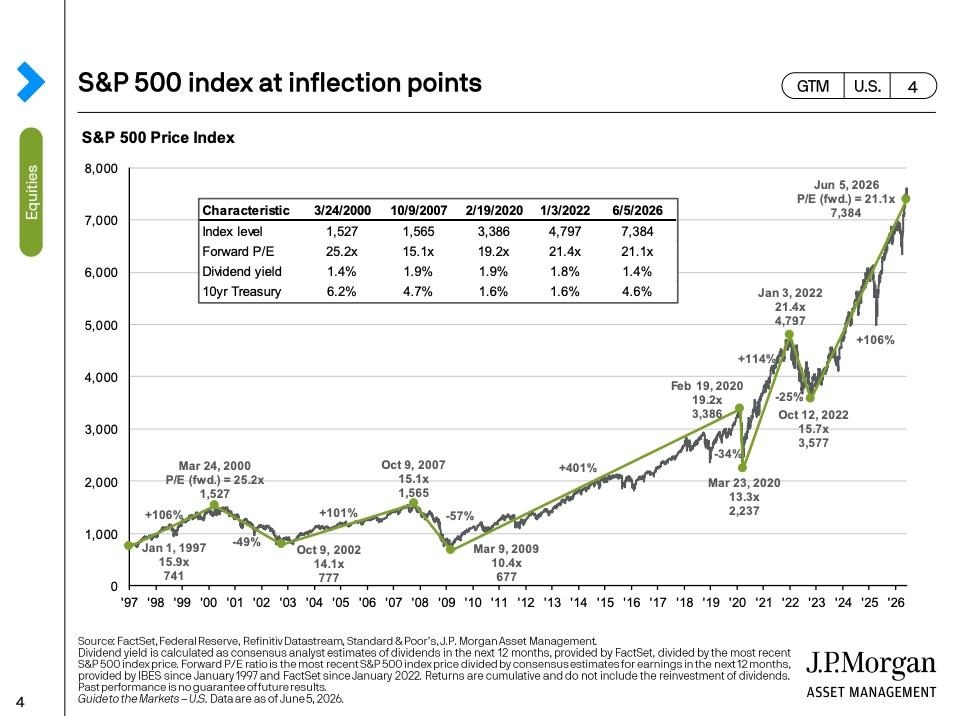

As we entered this quarter, markets were mostly flat on the year. Since then, we entered a war with Iran and saw a disruption in global oil flows. Naturally, that created some market instability and revived inflation fears. As mentioned in the last commentary, markets are resilient and tend to rebound in time. Not only did that happen again, but U.S. markets enjoyed roughly a 13% move higher after a 9% drop to start the quarter. As of this writing, CNBC is reporting the S&P 500 is up about 8.4% on the year.

How This Lines Up with Our 2026 Outlook

Much like our broader 2026 outlook, the main story has been earnings. This past quarter was phenomenal from an earnings standpoint, with forward earnings per share guidance among the best we have seen in a long time. That has moved our 2026 fEPS targets meaningfully higher and also improved the outlook for 2027. Due to those increases, we have raised our year-end S&P 500 target from around the 7,400 range to roughly 7,650 to 8,000. That still suggests additional upside from here if the fundamental picture continues to hold.

Macro Check-In: Inflation, Jobs, and Policy

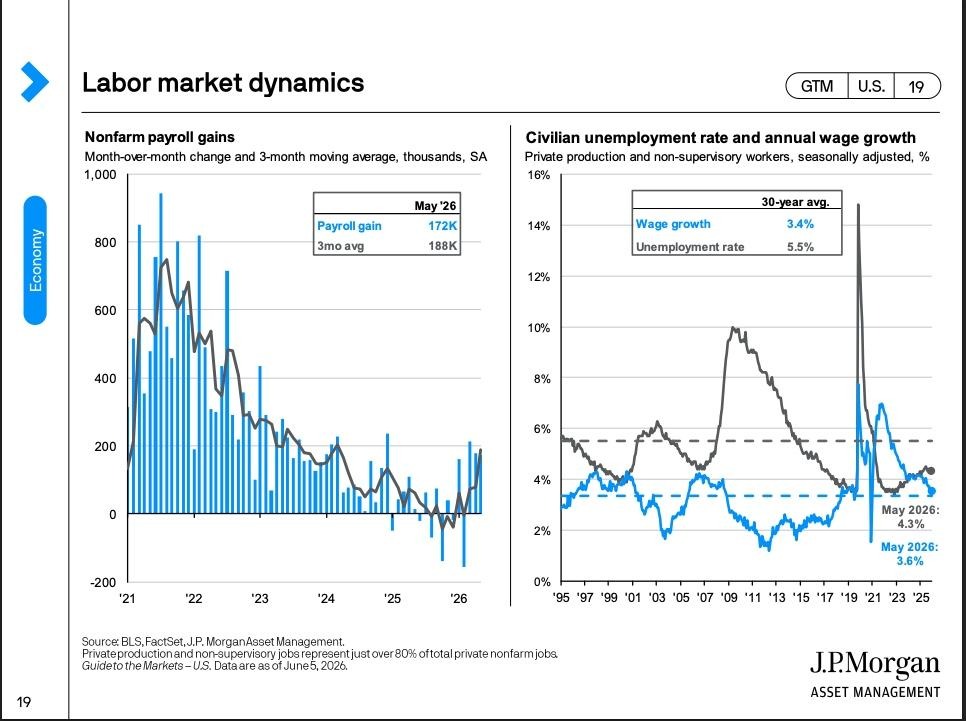

So what changed? Primarily, we have seen a large increase in tech company investment and spending related to the AI infrastructure boom. Along with that, the consumer has been very resilient, small- and mid-sized companies have become much stronger, and the last economic risk we have been writing about with employment does indeed appear to have bottomed. All good economic data points to a stronger environment than many expected.

While that is all good news, there are still negatives to point out. Namely, the ongoing conflict with Iran and the elevated oil prices that come with it. A short-term conflict likely would not elevate inflation permanently. The longer the situation goes unresolved, however, the more likely inflation becomes persistent. The good news is that we are not really seeing that in the data yet. The bad news is that it likely shows up if this drags on much longer.

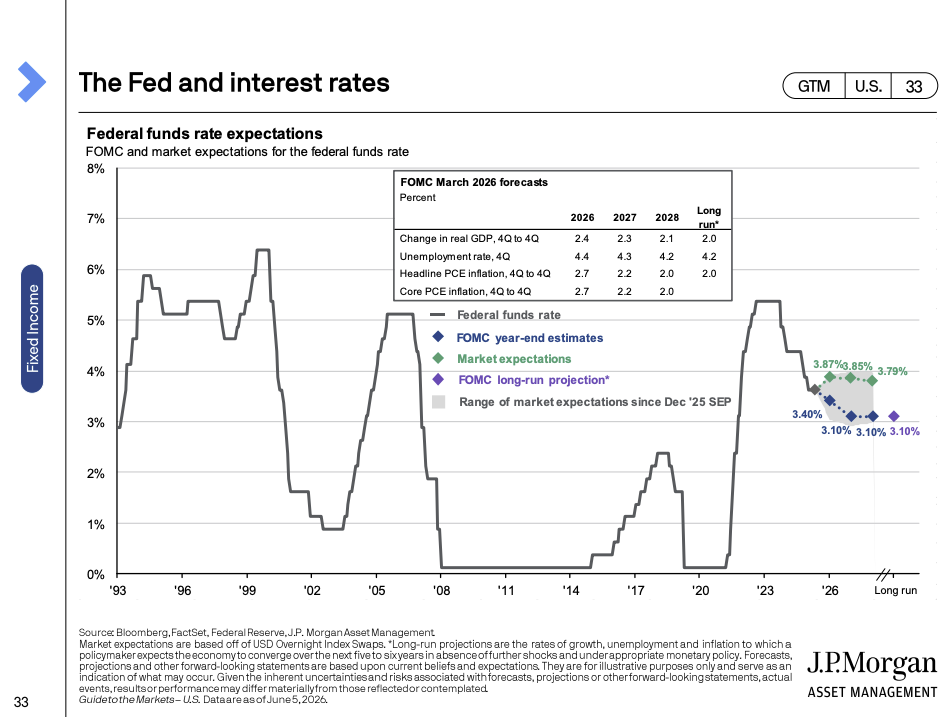

For that reason alone, there is a reasonable case that this conflict ends in the coming weeks, similar to why the tariff situation last year was expected to resolve quickly. The President does not want a bad economy on his record. With the rise in inflation concerns, markets have begun reading the situation as one where the Federal Reserve may not be able to reduce rates and may even need to keep rates higher for longer. That is contrary to what is believed here at this time. With new Fed leadership, comments made by the U.S. Treasury Secretary, and the broader policy backdrop, the preference still appears to be for a hotter economy that can outpace the debt scenario over time. To do that, rate cuts still likely need to be implemented in 2026.

What This Means for Portfolios

So what does this all mean for your portfolio? The data still suggests staying the course. There is still a lean into equities over bonds. However, that lean was reduced by approximately one-third of the overweight at the end of May. Across the various risk models, that meant reallocating a small percentage, around 5%, back into bonds after what we felt was a too-far-too-soon surge in the stock market.

Equities still appear to have room to grow into 2027, while the inflation and rate-cut risks have reduced the bond return projections for 2026 somewhat. Even so, those same factors may lead to a better second half for bonds than the first half if the Fed does reduce rates later this year and the Iran situation clears up sooner rather than later. As the difference between expected stock and bond returns narrows, the risk-reward tradeoff becomes a little more balanced.

While the risks have begun to shift from the 2026 outlook written last December, the long-term environment still looks constructive. The risks are still present, and the long-term rewards have come down slightly, but the overall view remains bullish with a longer period of growth ahead and an improving consumer and employment scenario.

Disclosure: Matthew Finley is an investment adviser representative with Savvy Advisors, Inc. (“Savvy Advisors”). Savvy Advisors is an SEC-registered investment advisor. The views and opinions expressed herein are those of the speakers and authors and do not necessarily reflect the views or positions of Savvy Advisors. Information contained herein has been obtained from sources believed to be reliable, but is not assured as to accuracy.

Resources

Related Posts

-

What to Do After a Large RSU Vesting (Taxes, Planning, and Next Steps)

Key Takeaways: Receiving a large amount of vested restricted stock units (RSUs) can be a major financial milestone. It can increase your net worth, create liquidity, and turn years of compensation into real value. However, it…

8 Min Read

By Matthew Nelson

July 14, 2026 -

How to Diversify When a Large Portion of Your Wealth Is in Company Stock

Key Takeaways: Company stock can become a major source of wealth for employees, founders, long-tenured professionals, and executives whose careers and compensation have been tied to one business. Over time, grants, ESPP purchases, option exercises, and…

9 Min ReadBy Matthew Nelson

July 6, 2026 -

Q3 2026 Market Outlook

Q2 of 2026 is shaping up better than we expected in our 2026 market outlook. Despite the noise around the globe and here in the U.S., based on CNBC-reported data, the S&P 500 is sitting roughly…

4 Min Read

By Matthew Finley

June 16, 2026